The Agentic Commerce Landscape: Who's Building What in 2026

Arjun Bhargava

Co-founder and CEO @ Rye

14 minutes read

Agentic commerce startups are building across 7 value chain layers — from AI platforms to trust infrastructure. A landscape map of 50+ companies, funding data, and where the gaps remain.

TL;DR / Key Takeaways

Agentic commerce isn't one product category — it's a 7-layer value chain, from AI platforms and protocols to checkout execution and trust infrastructure, with different companies, economics, and maturity at each layer.

The payments and identity layer is attracting the most startup funding, with Basis Theory, Nekuda, and Skyfire raising nearly $50 million combined to build the financial rails for agent transactions.

Checkout execution has surprisingly few pure-play companies despite being essential to every agentic transaction — most ecosystem energy has gone into discovery, protocols, and payments while the actual completion of purchases remains a bottleneck.

Six protocols (ACP, UCP, AP2, MCP, A2A, Visa TAP) are shaping how agents, merchants, and payments communicate — but every one of them requires merchant opt-in, leaving the long tail of millions of stores invisible to agents.

The market is projected to grow from $135 billion in 2025 to $1.7 trillion by 2030, with over 50 companies now building across the stack — yet the biggest gaps remain in universal merchant coverage and connecting product data to checkout execution.

Agentic commerce startups — alongside trillion-dollar incumbents — are assembling a new infrastructure stack in real time. Dozens of companies are building across at least seven distinct layers, each solving a different piece of the puzzle that lets AI agents discover, evaluate, and purchase products on behalf of consumers.

This isn't one product category. It's an emerging value chain — and the agentic commerce landscape looks very different depending on where you sit.

As a company building agentic commerce infrastructure — from real-time product data to checkout completion across the open web — we see both the rapid progress and the persistent gaps up close. This piece maps who is building what, where capital is flowing, and where the stack still has holes. (For a primer on what agentic commerce is and how it works, see our foundational guide.)

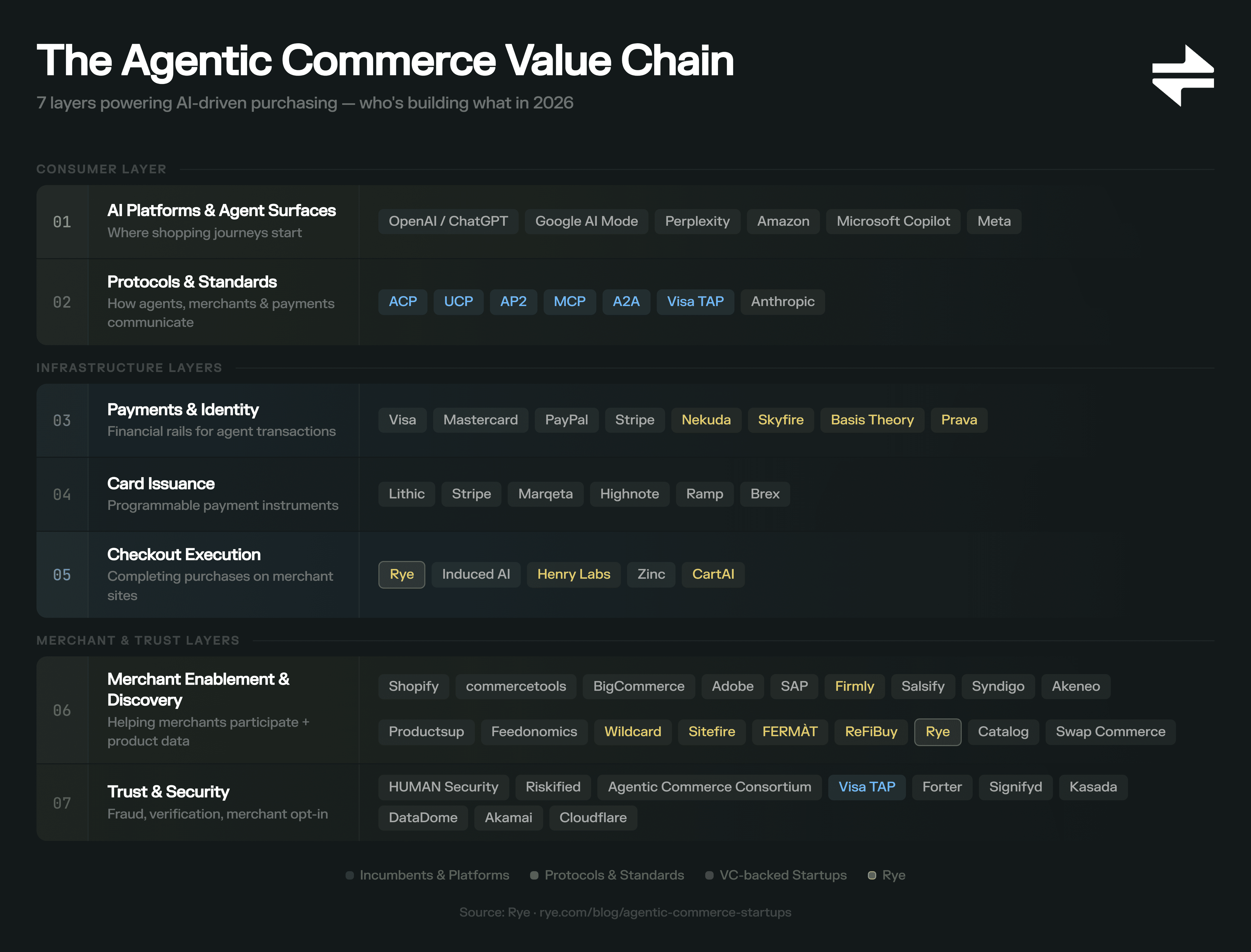

The Agentic Commerce Value Chain

Most landscape analyses treat agentic commerce as a flat category — a list of companies doing "AI shopping." But in practice, the stack has distinct layers, each with different economics, different players, and different maturity levels.

Here's how we map it:

Layer | Function | Key Players |

|---|---|---|

1. AI Platforms & Agent Surfaces | Where shopping journeys start | OpenAI / ChatGPT, Google AI Mode, Perplexity, Amazon, Microsoft Copilot, Meta |

2. Protocols & Standards | How agents, merchants, and payments communicate | ACP (OpenAI + Stripe), UCP (Google + Shopify), AP2, MCP (Anthropic), A2A, Visa TAP |

3. Payments & Identity | Financial rails for agent transactions | Visa, Mastercard, PayPal, Stripe, Nekuda, Skyfire, Basis Theory, Prava |

4. Card Issuance | Programmable payment instruments for agents | Lithic, Stripe, Marqeta, Highnote, Ramp, Brex |

5. Checkout Execution | Completing purchases on merchant sites | Rye, Induced AI, Henry Labs, Zinc, CartAI |

6. Merchant Enablement & Discovery | Helping merchants participate + product data | Shopify, commercetools, BigCommerce, Adobe, SAP, Firmly, Salsify, Syndigo, Akeneo, Productsup, Feedonomics, Wildcard, Sitefire, FERMÀT, ReFiBuy, Rye, Catalog, Swap Commerce |

7. Trust & Security | Fraud, verification, merchant opt-in standards | HUMAN Security, Riskified, Agentic Commerce Consortium, Visa TAP, Forter, Signifyd, Kasada, DataDome, Akamai, Cloudflare |

What makes this framework useful isn't the taxonomy itself — it's what it reveals about where activity is concentrated (payments and identity), where it's surprisingly thin (checkout execution), and where the biggest structural gaps remain (universal coverage across the long tail of merchants).

Let's walk through each layer.

The agentic commerce value chain — 7 infrastructure layers powering AI agent purchasing in 2026.

Layer 1: AI Platforms & Agent Surfaces

The consumer-facing AI platforms are where agentic shopping journeys begin — and they're moving fast.

OpenAI / ChatGPT launched Instant Checkout via the Agentic Commerce Protocol (ACP) in partnership with Stripe. ChatGPT now processes an estimated 50 million shopping-related queries per day, making it the largest AI-native commerce channel. Etsy was among the first merchants live, with over one million Shopify merchants initially in the onboarding pipeline. Product results are organic and unsponsored. PayPal has adopted ACP to expand merchant coverage further. OpenAI has since scaled back native checkout in ChatGPT, shifting to app-based purchases through integrated retailers like Instacart and Target after only ~12 merchants went live. For our analysis of what this means for checkout infrastructure, see our breakdown of the ChatGPT checkout pivot.

Google introduced agentic checkout in AI Mode and unveiled the Universal Commerce Protocol (UCP) at NRF 2026, co-developed with Shopify. The coalition already includes 20+ partners: Visa, Mastercard, Stripe, American Express, Target, Walmart, Wayfair, Etsy, Best Buy, Macy's, Home Depot, Adyen, Flipkart, and Zalando, among others. Google also launched the Agent Payments Protocol (AP2) to handle the payment authorization layer specifically.

Perplexity expanded Buy with Pro to all users via a PayPal partnership, connecting to over 5,000 merchants with in-chat checkout.

Amazon launched "Buy for Me" — enabling purchases from third-party retailers without leaving the Amazon app — and expanded coverage from roughly 65,000 to over 500,000 products. The company has simultaneously sued Perplexity over unauthorized agent-based purchasing on its marketplace, signaling a tension between participating in agentic commerce and defending its walled garden.

Microsoft Copilot is working with Mastercard to bring Agent Pay to Copilot Checkout, positioning Copilot as another distribution surface for agent-driven transactions.

Meta is the newest entrant. Mark Zuckerberg teased agentic commerce tools during Meta's January 2026 earnings call, describing "new agentic shopping tools" that will surface products from Meta's advertiser catalog. Meta acquired general-purpose agent developer Manus in December 2025, and has earmarked $115–135 billion in 2026 capital expenditures to support AI infrastructure.

For a deeper analysis of how these platforms are approaching agentic checkout, see our breakdown of big tech's agentic commerce strategies.

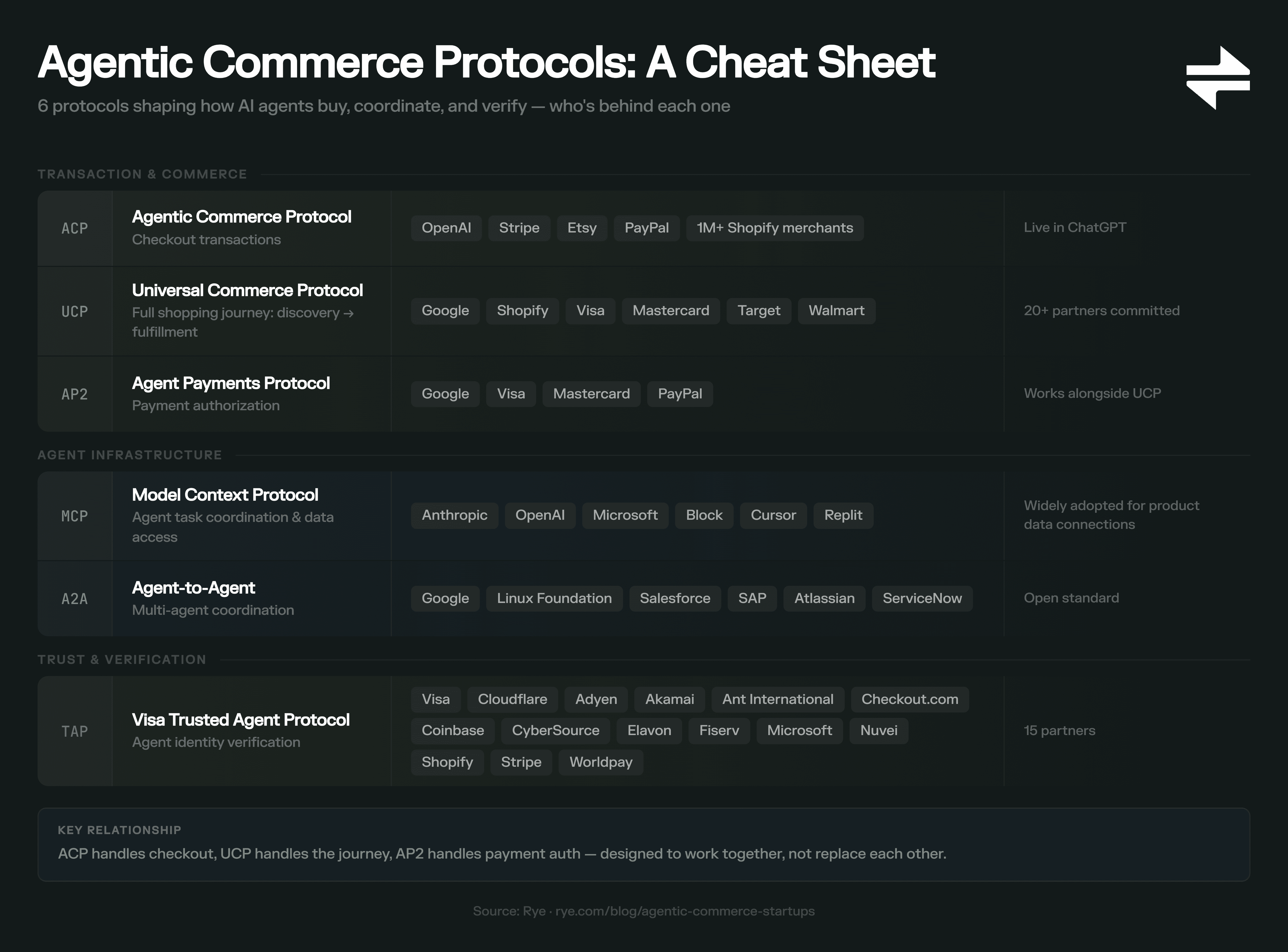

Layer 2: Protocols & Standards

Six protocols have emerged to govern how agents, merchants, and payment providers communicate — and they're more complementary than competing.

ACP (Agentic Commerce Protocol), developed by OpenAI and Stripe under Apache 2.0, defines how agents discover products, initiate checkouts, and complete purchases. It's live in ChatGPT today. UCP (Universal Commerce Protocol), co-developed by Google and Shopify, covers the full shopping journey from discovery through fulfillment and is platform-agnostic. AP2 (Agent Payments Protocol) from Google works alongside UCP for the payment authorization layer specifically, integrating with Mastercard, PayPal, and Visa. MCP (Model Context Protocol) from Anthropic provides foundational infrastructure for AI agents to coordinate tasks and access data — less commerce-specific but increasingly used for product data connections. A2A (Agent-to-Agent) from Google and the Linux Foundation enables multi-agent coordination. And Visa TAP (Trusted Agent Protocol) is an open framework to distinguish legitimate AI agents from malicious bots, with 10+ partners including Akamai.

The key observation: ACP handles checkout transactions, UCP handles the broader commerce journey, and AP2 handles payment authorization. They're designed to work together, not replace each other.

Agentic commerce protocols at a glance — who built each one, what it does, and where it stands today.

The critical gap: every one of these protocols requires merchant opt-in. Until a merchant actively integrates, their products remain invisible to protocol-compliant agents.

For a detailed breakdown of how these protocols work, see Section 7 of our agentic commerce guide.

Layer 3: Payments & Identity

This layer has attracted more startup activity and dedicated funding than any other — for good reason. Agent-initiated payments introduce entirely new requirements around identity verification, credential management, and fraud detection.

Visa launched its Intelligent Commerce platform with 100+ partners building against it, 30+ in sandbox, and 20+ agents integrating directly. Visa completed hundreds of secure, agent-initiated transactions in December 2025 and predicts millions of agent-completed purchases by holiday 2026. The company also developed the Trusted Agent Protocol (TAP) with 10+ partners to verify legitimate AI agents.

Mastercard rolled out Agent Pay to all U.S. cardholders in November 2025 and is working with Microsoft to bring it to Copilot Checkout. In January 2026, Mastercard expanded its Start Path accelerator to include a dedicated agentic commerce cohort and joined Google's UCP. At the center of Agent Pay are Mastercard Agentic Tokens — leveraging existing tokenization infrastructure to uniquely tie AI agents to individual users.

PayPal adopted OpenAI's ACP to expand merchant coverage in ChatGPT and published a merchant guide, "Making Sense of the AI Shopping Protocol Moment." PayPal is positioning itself as a single integration that distributes merchant catalogs across AI platforms — ChatGPT, Copilot, Perplexity — while keeping merchants as the merchant of record.

Stripe co-developed ACP with OpenAI and powers Instant Checkout in ChatGPT. In December 2025, Stripe launched the Agentic Commerce Suite — a turnkey solution rolling out via Wix, WooCommerce, BigCommerce, Squarespace, commercetools, Akeneo, and more. Early adopters include URBN (Anthropologie, Free People, Urban Outfitters), Etsy, Coach, Kate Spade, Ashley Furniture, and Revolve.

Three startups are building dedicated infrastructure at this layer:

Nekuda raised a $5 million seed round led by Madrona, with Amex Ventures and Visa Ventures participating. Nekuda's agentic payments SDK manages payment credentials and authorizations through two core components: Secure Agent Wallet and Agentic Mandates. The company is a launch partner for Visa Intelligent Commerce and is also building free ecosystem tools including Protocol Scout and Checkout.directory.

Skyfire has raised $9.5 million total from Neuberger Berman, a16z CSX, and Coinbase Ventures. Its KYAPay protocol ("Know Your Agent") uses signed JWTs for verified agent identity. Skyfire's Agent Checkout product processes thousands of transactions daily. A joint demo with Visa showed an AI agent autonomously purchasing a consumer product using KYAPay plus Visa Intelligent Commerce. Co-founder Amir Sarhangi previously sold Jibe to Google (the RCS messaging protocol).

Basis Theory raised a $33 million Series B led by Costanoa Ventures (approximately $50 million total), building a cloud-native, PCI-compliant, processor-agnostic vault. Basis Theory also leads the Agentic Commerce Consortium, a coalition of 20+ companies — including Lithic, Skyfire, Rye, Crossmint, NewGen, Henry Labs, Channel3, and Catalog — working to define standards for merchant-controlled AI commerce. Customers include Pinterest, Melio, and MoneyGram.

Prava provides a payments API that lets AI agents make secure, tokenized card-based purchases with passkey-based user approval — turning redirect links into native "buy now" buttons inside AI apps. Prava integrated with Visa Intelligent Commerce to enable card-based agentic payments in the U.S.

For more on how tokenization enables agentic commerce, see our deep dive.

Layer 4: Card Issuance

Agents need programmable payment instruments — virtual cards with custom authorization rules, spending limits, and real-time controls.

Lithic provides programmable virtual cards and is a member of the Agentic Commerce Consortium. (See our case study on Lithic and Rye's agentic checkout integration.) Stripe Issuing extends Stripe's presence from the payments layer into card issuance, offering programmatic virtual and physical card creation with real-time authorization controls — increasingly relevant as agents need purpose-built payment instruments. Marqeta and Highnote offer card issuing platforms with APIs for programmatic card creation and real-time authorization controls. Ramp has applied Visa Intelligent Commerce to automate B2B bill payments, while Brex provides corporate cards with programmatic controls for B2B agent workflows.

This is a "picks and shovels" layer — less visible than the platforms or protocols, but essential. Every agent-initiated purchase needs a payment instrument, and the card issuers providing programmable, API-first infrastructure are quietly powering transactions across the stack.

Layer 5: Checkout Execution

This is the "last mile" problem: once an agent has found a product and has payment credentials, it needs to actually complete the purchase on a merchant's site. And this is where the stack gets thin.

Rye provides a Universal Checkout API that lets any AI agent purchase from any online merchant using just a product URL and a tokenized payment method. No merchant integration is required. Rye recently launched its Product Data API for product discovery and is a member of the Agentic Commerce Consortium. Rye was also referenced in Visa's Intelligent Commerce pilot, where Nekuda partnered with fashion apps using Rye's checkout API for transaction execution. (For technical architecture details, see our Universal Checkout API whitepaper. For performance benchmarks, see our analysis of checkout latency and agent adoption.)

Induced AI operates browser automation for agent-driven commerce, taking a different architectural approach to the same last-mile challenge.

Henry Labs provides agentic one-click checkout for AI-native shopping interfaces, powered by Nekuda's wallet infrastructure SDK. Henry is integrated with platforms like Price.com and consumer apps including Aesthetic (myaesthetic.ai), enabling users to move from AI-styled discovery to completed purchase in a single flow. Henry is a founding member of the Agentic Commerce Consortium.

Zinc offers a purchasing API for major retailers including Amazon, Walmart, Target, and Best Buy, using managed retailer accounts to automate order placement, tracking, and returns. Originally built for dropshipping and fulfillment automation, Zinc has repositioned toward AI and agentic use cases — though its coverage remains limited to a handful of large retailers rather than the open web.

CartAI takes a publisher-and-affiliate-first approach to checkout execution, offering a white-label embeddable cart and checkout that lets content sites, influencer pages, and AI surfaces convert product mentions into completed purchases without redirecting users. CartAI supports merchant-native checkout across ACP, UCP, and browser agents, preserving attribution, loyalty accounts, and payment workflows. Founded by Manil Uppal — who previously built and sold Lash Delivery (acquired by H-E-B) and Delivery Solutions (acquired by UPS) — CartAI positions itself as "Agentic Commerce as a Service," bridging the gap between product discovery in content and checkout execution on merchant sites.

The execution layer has surprisingly few pure-play companies — a notable gap given that every agentic transaction eventually needs to complete on a merchant site. Most of the ecosystem's energy has gone into discovery, protocols, and payments, while the actual completion of purchases remains a bottleneck.

Layer 6: Merchant Enablement & Discovery

For agentic commerce to work, merchants need to participate — and AI agents need structured product data to work with. This layer is the broadest and most fragmented, spanning commerce platforms, product information managers, feed syndicators, and a new category of AI visibility tools.

Merchant Platforms

Shopify is the most aggressive platform mover. As co-developer of UCP with Google, Shopify has built a three-part agentic commerce stack: Catalog API (product data syndication), Universal Cart, and Checkout Kit. Agentic Storefronts — launched with the Winter '26 Edition — let merchants toggle on distribution to ChatGPT, Perplexity, and Microsoft Copilot from a single admin screen. Over one million merchants are onboarding to ACP. Notably, Shopify's new Agentic plan opens the Catalog to non-Shopify merchants for the first time, expanding the data backbone beyond its own ecosystem.

commercetools launched Agent Gateway, giving AI agents full product context through its API-first, headless architecture. Its Catalog Optimization Agent handles catalogs of 10M+ items.

BigCommerce (now rebranding as "Commerce") is unifying its platform with Feedonomics and Makeswift, offering headless APIs for agent interaction with storefronts, carts, and checkout. Feedonomics, its subsidiary, handles product data syndication (see below).

Adobe Commerce committed in February 2026 to supporting both UCP and ACP, expanding on its earlier AP2 commitment. Adobe's data shows AI referrals to storefronts convert 31% higher and generate 254% more revenue per visit than traditional traffic.

SAP unveiled a Catalog Optimization Agent at NRF 2026, scaling to 10M+ items with claims of 70% faster content improvement and 63% reduction in maintenance effort.

Protocol Aggregation

As protocols multiply, a new sub-layer is emerging: companies that abstract the complexity of ACP, UCP, AP2, and MCP into a single merchant integration.

Firmly ($5.2 million raised; investors include FJ Labs, Ark Invest, and Mastercard Start Path) launched a unified "Buy Now" platform in November 2025 that lets merchants sell across AI chatbots, social platforms, publishers, and connected TV through one integration — eliminating the need to implement each protocol separately. Firmly powers native checkout inside Perplexity's shopping experience and has partnerships with CJ (affiliate network) and Furniture.com. Merchants remain the merchant of record with zero engineering effort. BCG highlighted Firmly as a key infrastructure provider enabling "Commerce Everywhere." Founded by ex-Samsung executives and headquartered in Seattle, the company has been in stealth for five years before its Perplexity partnership brought it into the spotlight.

The Product Data Challenge

AI agents can't buy what they can't see. And product data is fragmenting into two camps: opt-in (merchant pushes data to agents) versus universal (agents pull data from any merchant).

On the opt-in side: Salsify launched an OpenAI Connect integration to share brand-approved content directly with ChatGPT. Syndigo launched both OpenAI Connect and a GEO (Generative Engine Optimization) product, publishing ACP-compliant product data covering IDs, nutrition, allergens, sustainability info, pricing, and availability across a network of 3,500+ retailers. Akeneo partnered with Stripe's Agentic Commerce Suite (announced February 2026) and launched an MCP Server connecting AI models directly to its product data. Feedonomics now distributes AI-enriched product feeds to agentic platforms. Productsup offers a live ChatGPT shopping integration via ACP.

On the analytics and visibility side: Wildcard (YC-backed) provides SKU-level visibility into how products appear inside ChatGPT and AI assistants. Sitefire (YC-backed) focuses on GEO, helping companies win customers on ChatGPT, Gemini, and other agents. ReFiBuy, founded by ChannelAdvisor creator Scot Wingo, offers an Agentic Commerce Optimization (ACO) platform — a Commerce Intelligence Engine that continuously evaluates, enriches, and monitors product catalogs for AI shopping agents, with Steve Madden as an early design partner. FERMÀT raised a $45 million Series B led by VMG Partners to build its "Commerce Brain" — a real-time shopper behavior graph that prepares brands for both human and agentic shoppers.

On the universal extraction side: Rye's Product Data API returns real-time, normalized product data from any merchant URL — no merchant integration required. (For details, see our Product Data API.) Catalog (getcatalog.ai), an Agentic Commerce Consortium member, structures product data for agent consumption. Swap Commerce combines a universal product catalog with a memory and preference layer.

The key tension: opt-in approaches cover the big merchants; universal approaches cover the long tail. Both will coexist. But agents that want to work across the entire open web — not just opted-in merchants — need both.

Layer 7: Trust & Security

The lightest layer in terms of dedicated startups, but among the most critical for scaling agentic commerce beyond early adopters — and it's gaining depth fast as the stakes become clearer.

Fraud and Identity

Forter launched Identity Monitoring for agentic commerce in August 2025 and has since proposed its own open-source Trusted Agentic Commerce Protocol for authenticating AI agents using JWS and JWE encryption. Across its network of 280,000+ merchants, Forter recorded an 18,510% day-over-day increase in agentic traffic within hours of ChatGPT Agent's launch — and has observed a 50% increase in fraud using scripted and automated attack modes. Its Agentic Orchestration Suite detects agent types, distinguishes legitimate AI agents from malicious bots, and links agent activity back to the consumer behind the agent. Signifyd is adapting its commerce protection platform for the dual-traffic reality, where merchants must evaluate both human-generated and agent-generated risk signals. Signifyd's CTO advocates for "parallel shopping universes" — separate experiences optimized for how humans and bots shop differently.

Bot Management and Edge Security

On the infrastructure side, bot management platforms are directly relevant to the challenge of separating legitimate AI shopping agents from fraudulent automation. Kasada and DataDome provide real-time bot detection and mitigation. Akamai brings edge-based behavioral intelligence — already a Visa TAP partner — while Cloudflare is building agent identification capabilities at the CDN layer. All four are adapting existing bot management infrastructure for a new reality where some automated traffic is desirable.

Standards and Verification

HUMAN Security partnered with Riskified to deploy the AgenticTrust platform, addressing the specific fraud patterns created by AI agent shopping — where automated purchasing behavior can resemble bot attacks. The Agentic Commerce Consortium, led by Basis Theory with 20+ members, is defining merchant opt-in standards, working on authorization and verification frameworks, product catalog discovery protocols, and unified shopping cart APIs. Visa TAP provides the agent verification framework that lets merchants distinguish between legitimate AI agents and malicious actors.

For more on consumer trust, fraud detection, and security in agentic commerce, see our dedicated analysis.

Where Agentic Commerce Capital Is Flowing

The funding landscape reveals where investors see the biggest opportunities — and the biggest gaps.

Company | Amount | Round | Date | Lead Investor(s) |

|---|---|---|---|---|

Basis Theory | $33M | Series B | Oct 2025 | Costanoa Ventures |

FERMÀT | $45M | Series B | Jun 2025 | VMG Partners |

Nekuda | $5M | Seed | May 2025 | Madrona + Amex/Visa Ventures |

Skyfire | $9.5M | Seed + follow-on | Aug–Oct 2024 | Neuberger Berman, a16z CSX, Coinbase Ventures |

Three patterns stand out. First, the payments and identity layer is attracting the most dedicated startup funding — Basis Theory, Nekuda, and Skyfire have collectively raised nearly $50 million to build the financial infrastructure for agent transactions. Second, the merchant enablement layer is dominated by platform extensions (Shopify, commercetools, BigCommerce) rather than new startups — incumbents are adding agentic capabilities to existing products rather than ceding the market to new entrants. Third, the checkout execution and universal product data layers have surprisingly few pure-play startups, despite being essential to any agentic transaction that crosses the boundaries of a single merchant ecosystem.

The broader market context: Edgar, Dunn & Co projects the agentic commerce TAM at $135 billion in 2025, growing to $1.7 trillion by 2030 — a 67% CAGR. McKinsey estimates AI agents could mediate $1 trillion in U.S. retail alone by decade's end. Adobe reports that AI shopping queries grew 4,700% between July 2024 and July 2025. Visa reports a 1,200% year-over-year increase in traffic to retail sites from AI agents. The investment thesis is straightforward: infrastructure companies that become embedded in this transaction flow early will be difficult to displace later.

What's Still Missing in the Agentic Commerce Stack

Despite the rapid buildout, three structural gaps remain.

The universal coverage gap. Every protocol — ACP, UCP, AP2 — requires merchants to opt in. Platform catalogs (Shopify, commercetools) cover their own merchants. Feed syndicators (Salsify, Syndigo, Akeneo) cover enterprise brands who actively push data. But the vast majority of online merchants — the long tail of millions of stores — remain invisible to protocol-compliant agents. Until this gap closes, agents can only shop a fraction of the open web.

The data-to-checkout gap. Most product data solutions are decoupled from transaction capability. You can use Syndigo to discover product information and Stripe to process a payment, but connecting the two requires separate integrations. Very few companies pair product discovery with checkout execution in a single integration — which means agents building cross-merchant shopping experiences need to stitch together multiple APIs.

The fragmentation problem. An agent building a cross-merchant shopping experience today needs to integrate with Shopify Catalog for Shopify merchants, ACP feeds for ChatGPT-connected merchants, a scraping API for Amazon, and individual merchant APIs for everyone else. There is no single integration that covers the full breadth of the open web — from the largest retailers to the smallest Shopify stores to the independent merchants running on custom platforms.

The Agentic Commerce Stack: Looking Ahead

The agentic commerce stack is being assembled in parallel by dozens of companies, each building a piece of an infrastructure that didn't exist two years ago. The next 12–18 months will determine which layers consolidate and which remain fragmented.

What's clear already: the companies that win will be those that embed themselves in the transaction flow early — becoming the infrastructure that agents rely on to discover products, verify identity, execute payments, and complete purchases. The protocols are converging. The payments rails are being built. The platforms are onboarding millions of merchants.

The question that remains is who will serve the rest — the long tail of merchants that no single protocol or platform covers today. That's where the next wave of infrastructure is being built.

For a foundational understanding of agentic commerce and how this stack fits together, see our guide to agentic commerce.

Frequently Asked Questions

What is the agentic commerce value chain?

The agentic commerce value chain is a 7-layer framework that maps the infrastructure required for AI agents to complete purchases on behalf of consumers. The layers are: (1) AI Platforms & Agent Surfaces, (2) Protocols & Standards, (3) Payments & Identity, (4) Card Issuance, (5) Checkout Execution, (6) Merchant Enablement & Discovery, and (7) Trust & Security. Each layer has different economics, different players, and different maturity levels — with payments attracting the most startup funding and checkout execution having the fewest pure-play companies.

Where is venture capital flowing in agentic commerce?

Venture capital in agentic commerce is concentrated in the payments and identity layer, where Basis Theory, Nekuda, and Skyfire have raised nearly $50 million combined. The merchant enablement layer is dominated by platform extensions from Shopify, commercetools, and BigCommerce rather than new startups. The checkout execution and universal product data layers have surprisingly few dedicated startups despite being essential to cross-merchant agentic transactions.

What protocols are used in agentic commerce?

Six major protocols govern agentic commerce as of 2026: ACP (Agentic Commerce Protocol) from OpenAI and Stripe handles checkout transactions, UCP (Universal Commerce Protocol) from Google and Shopify covers the full shopping journey, AP2 (Agent Payments Protocol) from Google handles payment authorization, MCP (Model Context Protocol) from Anthropic provides foundational agent infrastructure, A2A (Agent-to-Agent) from Google enables multi-agent coordination, and Visa TAP (Trusted Agent Protocol) verifies legitimate AI agents. These protocols are complementary rather than competing, but all require merchant opt-in.

How many companies are building in agentic commerce?

As of early 2026, over 50 companies are actively building agentic commerce infrastructure across the value chain. This spans AI platforms, payment networks, dedicated startups, commerce platforms, and trust and security providers. CB Insights has mapped 90+ companies in the broader space. Activity is concentrated in payments and identity infrastructure, while checkout execution and universal product data remain underserved relative to their importance in the stack.